Are you struggling with unmanageable debts? Have you been issued with a County Court Judgment, CCJ, by your creditors?

Receiving a County Court Judgement can be concerning but you can have a CCJ Discharged.

This will make sure your credit file isn’t negatively impacted.

In this article, we will explore what exactly CCJ Discharged entails, what will happen once your CCJ has been labelled as discharged, and any other important questions surrounding County Court Judgements.

Table of Content

- 1 What is a County Court Judgement (CCJ)?

- 2 Where can I find details of my CCJ?

- 3 Are CCJs a matter of public record?

- 4 What does CCJ Discharged mean?

- 5 What happens when my CCJ is discharged?

- 6 What if I can’t pay the County Court Judgement (CCJ) within the month?

- 7 How long does a CCJ stay on your credit report?

- 8 How much does a County Court Judgement affect my credit file?

- 9 Can you get a discharged CCJ removed from your credit file?

- 10 My County Court Judgement has been Discharged, can I still get financial help for my debts?

- 11 What debt solutions are there in place to help me get out of debt?

- 12 The Journey of Debt

- 13 Summary

What is a County Court Judgement (CCJ)?

Firstly, it is important that you understand what a County Court Judgment is before we move on to explain how you can get one discharged.

If you refuse to or cannot pay your debts back to any creditors, then a CCJ may be taken out by your lenders, in an attempt to reclaim their money.

Your lenders will send their application through to the court explaining why they believe a CCJ is the only logical solution.

Essentially, a CCJ is a court order which forces people to pay back any money owed to their creditors.

You can request a copy of your credit report from your credit reference agency if you want to check if you have a CCJ out against you.

As soon as you realise you will struggle to repay any of your debts, you should seek out free debt advice from a professional financial advisor.

Where can I find details of my CCJ?

You can find where a CCJ is registered on a public database called the Register of Judgements, Orders and Fines.

This public register includes important information, such as the finer details of the CCJ agreement.

Being served with a County Court Judgement can have a negative impact on your credit rating and credit file.

With that in mind, it is best that you do everything possible to avoid being issued with a CCJ.

Are CCJs a matter of public record?

The Register of Judgements, Orders and Fines is a public document.

As it is a public register, anyone can request to receive information stored on the database.

The information that can be dispersed, off of the register, is as follows:

- Your name

- Your address

- The case number

- The court that sent the CCJ

- The amount of money you owe

It may be concerning that anyone can simply use the log and see your details.

However, it’s likely only creditors, letting agencies and employers who will be interested, as they may need to know about your financial history.

What does CCJ Discharged mean?

Once you receive a CCJ, don’t panic!

There are ways to make amendments before your credit score is impacted. This is known as a CCJ Discharged.

A CCJ Discharged means that your CCJ will be dropped as you have paid up all your debts.

You can only access a CCJ Discharged if your debts are paid in full within one calendar month of the County Court Judgement being assigned.

What happens when my CCJ is discharged?

Once you have fully paid off your loans, you then need to give the court evidence to prove you have settled your debt.

They will want to check the money you owe was paid before the CCJ Discharge cut off date.

If you have paid before the deadline, the court will then inform the Registry Trust and the debt will be wiped from your records.

What if I can’t pay the County Court Judgement (CCJ) within the month?

If you are unable to repay your debts within the one-month limitation, you can still pay them off when possible.

However, this will not be classed as CCJ Discharged and the County Court Judgments will not be removed from your credit file.

Once you pay off your County Court Judgement it will be marked as ‘satisfied’.

How long does a CCJ stay on your credit report?

A CCJ will be documented on your credit report for at least six years.

So, due to your credit report’s public nature, any of your lenders who choose to run a credit check will be able to see details of your CCJ.

Having a CCJ on your credit file might highlight your difficult financial past, which can make it harder to open bank accounts, take out a mortgage or acquire a loan.

Remember, there is a solid link between a weak credit report and a low credit rating.

So, it is important to always try and avoid having a County Court Judgement issued, as this can make other aspects of your finance much more difficult as well.

If you manage to get a CCJ discharged, it will be automatically removed from the register, and you can apply for it to be removed from your credit report.

If you can’t get your CCJ discharged, after six years the CCJ will be removed from your credit file altogether.

How much does a County Court Judgement affect my credit file?

If you have a CCJ on your credit report, this will suggest to creditors that you are not reliable in repaying loans on time.

Lenders, such as those who provide mortgages, will be hesitant to take you on, as they might not trust your ability to keep up with your monthly instalments.

More often than not, if you have a CCJ on your credit history, then your application for most loans will be rejected.

Can you get a discharged CCJ removed from your credit file?

Once you have successfully paid off your debts, within the one month period, you can then get your CCJ removed from your credit report.

The discharged CCJ will be taken off the public register straight away. It is after this time that you can then apply to have it removed from your credit records.

You can do this by sending off an application for a ‘certificate of satisfaction’ to your county court.

To do this, you will need an N443 claim form, which is available to download for free off of the governments’ official website.

Once the court in question has received evidence of the fully paid debt, they will remove the CCJ from any public records and your credit file.

It is important to allow the credit reference agencies some time to update your refreshed information.

My County Court Judgement has been Discharged, can I still get financial help for my debts?

It is a great feeling having your County Court judgment CCJ discharged, as it means you have paid the full amount of your court-appointed debts.

However, this might not cover all of the outstanding debt that you owe to various lenders.

You may still need to repay money and find a debt solution that works for you.

Don’t worry, even if you have had a CCJ, you can still access free debt advice from professional financial advisers and debt charities.

They will be happy to help you if you are struggling with debt and will work with you to find the best way to financial freedom.

What debt solutions are there in place to help me get out of debt?

If you are ready to tackle your debts and start your journey to financial freedom, then you should explore the following debt solutions.

Debt charities can offer free advice as to which solution may be the best for your unique financial circumstances.

Individual Voluntary Arrangement (IVA)

An IVA is a government scheme that aids you in repaying your creditors.

Under an IVA agreement, you will make a payment each month to an insolvency practitioner.

The insolvency practitioner will then direct a proportion of your payment to the relevant lenders.

Any interest rates or charges will be frozen while you are making repayments under an IVA.

An IVA is possible provided the lenders who own at least 75% of your debts agree to this type of arrangement.

Remember, if you fail to make your IVA repayments, then your insolvency practitioner can file you as bankrupt.

Missed payments can plunge you further into hot water, so make sure you only take out an IVA if you can meet your monthly instalments.

Debt Consolidation

A debt consolidation loan allows you to move existing debts or loans to one place, which makes it easier to manage your finances.

Typically, people choose to move their store cards, credit cards, or other bank account loans within a debt consolidation agreement.

You would borrow money to cover all your outstanding debt, then you would owe lower monthly repayments to one creditor, rather than many.

Be careful, as these types of agreements can result in you paying more money than you initially owed.

Debt Management Plan (DMP)

A debt management plan, or DMP, is an agreement that is set up between the debtor and their lenders, which allows them to lay out a clear plan for repayment.

A debtor will make reasonable monthly repayments, to a debt management company, until the loan has been paid in full.

Bear in mind that the debt management plan can be cancelled at any point should you fail to make your monthly repayments.

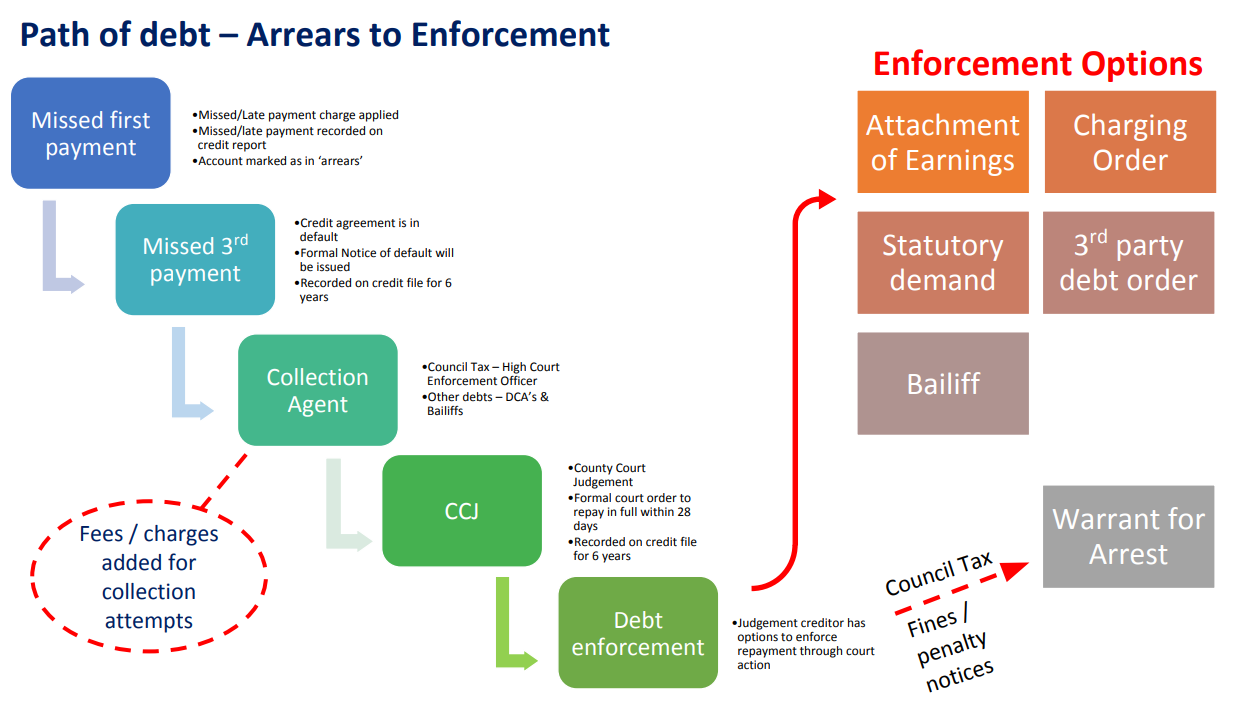

The Journey of Debt

Here is the path of debt – from arrears to enforcement.

- Missed First Payment – Marked as in ‘arrears’

- Missed 3rd Payment – Formal Notice of Default

- Collection Agent

- CCJ – County Court Judgement

- Debt Enforcement – Attachment of Earnings

- Debt Enforcement – Charging Order

- Debt Enforcement – Statutory Demand

- Debt Enforcement – Warrant for Arrest

- Debt Enforcement – 3rd Party Debt Order

- Debt Enforcement – Bailiff

Summary

A CCJ isn’t something that you want to have taken out against you, but you may not have been able to avoid it.

It can be scary, stressful and you might not know which direction to go in.

You can get a CCJ discharged if you are able to repay all the funds owed in the allocated one month period.

This means the CCJ will be removed from your credit report and the public register!

If you can’t, it’s not the end of the world. You can find many different debt solutions by speaking with a professional debt advisor.

Contact a debt help charity today, as they will be more than happy to help you! You can access free debt advice.