If you have had bailiffs knocking on your door and demanding payments, you might be confused and concerned.

You might even be wondering if these bailiffs can get a warrant for arrest over debts.

This article will cover all there is to know about what bailiffs can and cannot do as they attempt to reclaim the outstanding debt.

Keep reading to find out how to make a complaint about unfair or threatening debt collectors.

Table of Content

- 1 Can bailiffs issue an arrest warrant?

- 2 Can I go to prison for outstanding debt?

- 3 Are there any situations where debts could lead to prison?

- 4 What happens when a bailiff comes to collect money?

- 5 Do bailiffs come with police?

- 6 Can bailiffs force entry to my premises?

- 7 What happens if I have nothing for bailiffs to take?

- 8 Can I trust the bailiffs to be honest?

- 9 How do I make a complaint about a debt collection agency?

- 9.1 If the bailiff is privately employed and enforcing magistrates’ court fines

- 9.2 If the bailiff is collecting money for a council or Transport for London (TfL)

- 9.3 If the bailiff is a member of a trade organisation

- 9.4 If the bailiff is a high court enforcement officer

- 9.5 If the bailiff is a court bailiff

- 10 Debt Solutions

- 11 Summary

- 12 The Journey of Debt

Can bailiffs issue an arrest warrant?

No, commercial bailiffs are not permitted to issue arrest warrants, arrest or restrain any individual, even if they have not paid their outstanding debts.

Bailiffs can issue a no-bail warrant under section 117 of the Magistrates Courts Act 1980, which is a warrant that is used to attempt to confirm bail.

A no-bail warrant is usually taken to try and locate a debtor and their current address, rather than to arrest them.

However, approved enforcement agents might be able to arrest you, if you have a warrant out for your arrest for breaking a community penalty order.

You can be sent to prison for up to 3 months if the court decides you don’t have a good reason to not pay your Council Tax and you refuse to do so. In order to be sent to prison the magistrate must be convinced that you have either ‘wilfully refused’ to pay the tax or you have been ‘culpably neglectful’ which means you have had the means to pay but have simply neglected to pay . You will receive a Summons to appear before the magistrates to explain why you should not be committed to prison.

Remember, it is illegal for bailiffs to pretend that they have legal powers which in fact they do not, so make sure to check their identity and learn what rights you have.

Can I go to prison for outstanding debt?

It is highly improbable that you would be arrested or sent to jail as a result of outstanding debt.

There are certain cases, such as with priority debt, where theoretically, you could be sent to jailed or fined for lack of payment.

Priority debts include:

- Criminal fines

- Council tax

- Child maintenance arrears

- Business rates

However, even with priority debts, the chances of you being arrested for missed payments are minimal and would only be the last resort.

For other non-priority debts, such as credit card, catalogue, mortgage and utility arrears, there is no possible way of you being arrested or sent to prison for missed payments.

Find Out The Best Debt Solution Bespoke To Your Financial Situation

30 Second Debt Assessment QuizAre there any situations where debts could lead to prison?

There are some very rare circumstances in which you could be arrested and taken to court or jail due to outstanding arrears.

For example, if you continuously miss CCJ payments and choose to ignore letters from the court, then a bailiff may be sent to your property to collect you and take you to court.

The court may then decide to send you to jail for up to 14 days, however, this punishment is for disobeying court orders, not missing debt repayments.

It is important to remember that it is only priority debts where there is a slight potential of a bailiff being sent for your arrest. If a bailiff suggests they have the power to arrest you over non-priority debts, then they are not being honest and you should write a formal complaint.

What happens when a bailiff comes to collect money?

If you have outstanding debt, there may come a time when you get a knock on the door from a bailiff.

The bailiff visits tend to happen in an attempt to reclaim the money owed, but there are a few things you should be aware of before complying with the bailiff’s requests.

Check the bailiff’s identity

First things first, always make sure to ask the bailiff for valid identification before making any payments or engaging in further conversation.

You can check the bailiff’s identity by asking for the following:

- Valid ID, such as their agent ID or enforcement agent certificate.

- Proof that they work for the company they say they do.

- A telephone contact number to confirm their details.

- A breakdown and evidence of the amount you supposedly owe.

If the bailiff at your door cannot provide evidence of their identity or the company they work for, then do not let them into your property or pay them any money.

You should turn them away and explain that you will only deal with them once they can provide you with a valid certificate.

Check what kind of enforcement agent they are

You should also be aware of the many different types of bailiffs, and what powers they hold:

- Certificated enforcement agents, otherwise known as civil enforcement agents.

- High court enforcement officers.

- County court and family court bailiffs.

- Approved Enforcement Agents, otherwise known as civilian enforcement officers.

The only enforcement agents that can issue arrest warrants or issue magistrates’ court fines are Approved Enforcement Agents.

An Approved Enforcement Agent can arrest you provided there is a warrant against you for breaking a community penalty order.

You can check they are the specific enforcement agent they say they are by the following methods:

- Certificated enforcement agent – check the register of certificated bailiffs.

- High court enforcement officer – check the register of court enforcement officers.

- County court and family court bailiffs – contact the court from which they have been sent.

- Approved Enforcement Agent – check they are from either Compliant Data-Led Engagements & Resolutions (CDER) Group, Marston Holdings Limited, Excel Civil Enforcement Limited or Swift Credit Services Limited.

Do I have to let the bailiffs in my home?

You do not have to let a bailiff into your home or property. Bailiffs cannot enter your home:

- By forced entry, meaning they cannot use force to enter your home if you have not given them permission.

- If there are children under the age of 16 or there are vulnerable individuals present.

- If they arrive between 9 pm and 6 am.

- Through any entrance other than the front door, so they cannot try to gain entry through windows.

The only exception which may permit a bailiff to force entry into your home is to collect unpaid priority debt, such as criminal fines, Income tax, or stamp duty.

Even still, forced entry will be the last resort and enforcement agents are not typically allowed to force entry into a property.

Should I make a payment?

You should try and make your outstanding debt payments before a bailiff gets sent to your home. However, if a bailiff does come demanding payment, first check their identification before making a payment.

You want to make sure that the debt they are attempting to make you pay is definitely yours.

If you can pay them there and then, you still don’t need to let them in your home, you can make a payment on the doorstep.

Should you not be able to make full repayment, you can try and sort out a payment arrangement with the bailiff which might allow you to make monthly instalments until the debt is paid off.

Can they take my belongings?

If you let a county court bailiff, family court bailiff, or civilian enforcement officer into your home and refuse to make a payment arrangement or an upfront payment for the debts you owe, then they may try to claim some of your possessions as collateral.

Bailiffs will try and take belongings or luxury items with significant value, such as televisions. However, they are not permitted to take the following items:

- Things of essential use, such as clothes, fridges or cooking appliances.

- Any tools or equipment needed for work that cost less than £1,350 altogether.

- Someone else’s possessions, such as items that may belong to your husband or joint tenant.

If you argue that the items the bailiffs are attempting to take are not yours, then you will need to provide them with evidence.

If you refuse to permit the bailiff’s entry to your house, then they might try and claim possessions that are outside, such as cars. To avoid repossession of your vehicles, always make sure to park them indoors or at a friend or family’s home.

Do bailiffs come with police?

Bailiffs do not need to be accompanied by a police officer when they make house visits, however, if you feel a bailiff is threatening or taking action outside of their power, then you might can to call the police.

There are strict rules that bailiffs have to follow, such as they are not allowed to force their way into a home.

You can and should call the police if a county court bailiff, or any other form of enforcement officer, is doing the following:

- Threatening you.

- Attempting to force entry.

- Attempting to enter your property through a window.

- Verbally or physically assaulting you.

Police officers can assess whether the bailiff has acted within their lawful right and if they feel the bailiff has misconducted themselves, they will assist you in removing them from your property.

Can bailiffs force entry to my premises?

No, bailiffs are not lawfully permitted to force entry to your property if you have not given them permission.

You should receive an enforcement notice at least seven days before a bailiff visits your property, making you aware of the enforcement action that will follow.

What happens if I have nothing for bailiffs to take?

If the County Court bailiffs are unable to claim any owed money or belongings, then they may have to refer back to the original creditor.

In the case of non-payment, the creditor may then take further action to reclaim the money they are owed, such as contacting the court.

If the court agrees, then you may be forced to file for bankruptcy, or in severe cases, you may even be sent to court and face imprisonment or fines.

Can I trust the bailiffs to be honest?

It is considered fraud if a bailiff pretends to possess powers which they actually do not, however, this does not always mean they will be honest with you.

If you have fallen into any kind of debt trouble, it is important to seek out professional debt advice.

A qualified debt advisory service will be able to help you understand how to deal with bailiffs and what powers they possess.

If you feel that the bailiff action you have experienced has been dishonest, for example, if a County Court bailiff has told you they have a warrant for your arrest, then you should file a formal complaint or contact the police.

How do I make a complaint about a debt collection agency?

If you wish to make a complaint about a bailiff that has misconducted themselves, you first need to find out if they are privately employed.

If the bailiff is privately employed and enforcing magistrates’ court fines

If a bailiff is privately employed and enforcing magistrates’ court fines, you should send your complaint directly to the company that they work for.

You should include the bailiff’s ID card number, details about your experience with them, and your contact details.

You should also send a complaint to the court from which the warrant was sent, to make them aware that misconduct has taken place.

If the bailiff is collecting money for a council or Transport for London (TfL)

If the bailiff is collecting money for your local authority, council, or the Transport for London, then you should contact the council directly to make your complaint.

If you do not feel like the council has resolved the matter appropriately, then you can escalate your complaint to the local government or the Social Care Ombudsman (SCO).

If the bailiff is a member of a trade organisation

If the bailiff is a member of a trade organisation, then you can send a complaint through to the trade association they are with.

You can check memberships on the CIVEA list, and the HCEOA directory, or contact the CEAA to check the membership status.

Each association has a unique complaints procedure, so make sure to check how to send a complaint via their websites.

If the bailiff is a high court enforcement officer

If the high court enforcement agent has seriously misconducted themselves, you can reach out to the high court and see if they would consider disbarring the bailiff.

You should send a letter to the following address:

Civil Enforcement Policy

Civil Law and Justice Division

Ministry of Justice

102 Petty France

London

SW1H 9AJ

Your letter should include details and evidence of the bailiff’s misconduct, and a return address so that if the court should wish to escalate the complaint they have your details to gain further information.

If the bailiff is a court bailiff

If the bailiff is a civilian enforcement officer, then you should send your complaint through to the court from which they were sent.

The bailiff is entitled to provide you with which court has sent them. Usually, it will be your local court, but if it is not, you should find out which specific court has sent them for the first visit.

Do Not Speak to Debt Solicitors Until You Know About This?

Find Out MoreDebt Solutions

When analysing your credit report and current debtors it is advised to understand all the debt solutions available to you.

Here are all the UK debt solutions available to you depending on where you are based in the UK:

- Best DAS Companies

- Best Full and Final Companies

- Best IVA Companies in Manchester

- Best IVA Companies UK

- Best Sequestration Companies

- Best Trust Deed Companies

- Debt Consolidation Companies

- Debt Relief Order Companies

- DMP Companies

Summary

To conclude, if a bailiff visits you, it will usually be because you owe money to a creditor.

However, in some cases, a bailiff might suggest that they have a warrant for your arrest. In the majority of cases, this is not correct and you should be wary.

A commercial bailiff is not permitted to make any arrests and they will not be sent with a warrant for your arrest.

An approved enforcement agent may be sent with a warrant for your arrest provided you have broken a community penalty order.

Make sure the enforcement agent provides you with evidence of the warrant before you comply and always check their identification to make sure they are being honest about who they say they are.

Did You Know You Can Write Off Up To 85% Of Your Debts?

Do I Qualify?The Journey of Debt

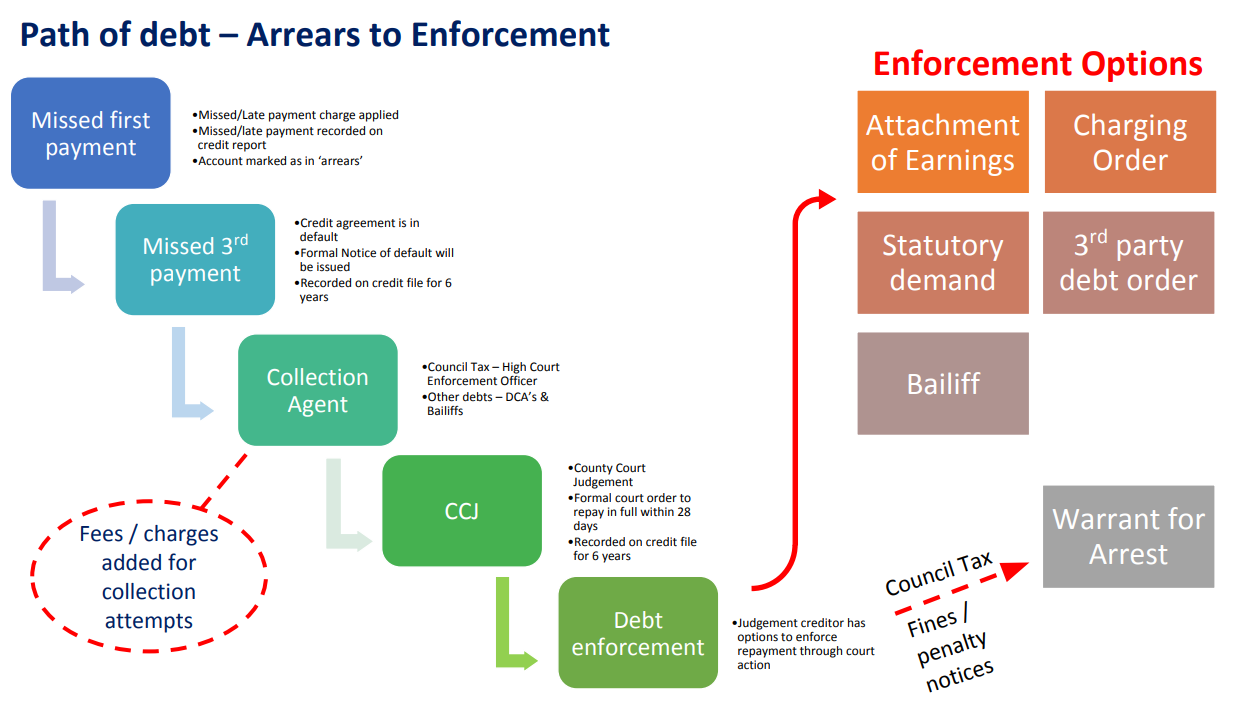

Here is the path of debt – from arrears to enforcement.

- Missed First Payment – Marked as in ‘arrears’

- Missed 3rd Payment – Formal Notice of Default

- Collection Agent

- CCJ – County Court Judgement

- Debt Enforcement – Attachment of Earnings

- Debt Enforcement – Charging Order

- Debt Enforcement – Statutory Demand

- Debt Enforcement – Warrant for Arrest

- Debt Enforcement – 3rd Party Debt Order

- Debt Enforcement – Bailiff